The monthly deposit of interest-free money into a savings account is a rare and welcome event. Putting funds in a bank account earns you interest, so it makes sense to do so. The question is, how much attention can you expect to receive? Learning how to calculate your profits from a savings account is useful regardless of where you choose to store your money since the answer changes based on your commercial bank and a few other criteria.

A Savings Account: What Is It?

If you don't intend on spending the money right away, you should put it in a savings account. This is not the same as a checking account, which is a transactional account designed for routine purchases and cash withdrawals at ATMs. To save money for later use or to reach a future goal, people often open savings accounts. A savings account might well be used for a variety of purposes, such as storing money for a rainy day or a house deposit. It's true that you may access your savings whenever you need to, but keep in mind that many financial institutions have restrictions on the number of times you can access your money.

What Is Interest?

To put it simply, interest is what you pay when you borrow or lend money. Interest is paid on borrowed money, such as a car loan or mortgage. However, whether you place funds in a savings account that earns interest or any other account, you are basically lending those funds to the financial institution holding the account. Banks use your money and pay you interest for the privilege. It then "borrows" that sum and uses it to finance the purchases of automobiles, homes, and other consumer goods for other people. There may seem to be a great deal of money being lent and borrowed, but keep in mind the following: You are paid by the bank just for trusting them with your savings when you put them in an interest-bearing account.

Interest types: Simple vs. Compound

Simple interest & compound interest are the two most common types of interest. Compound interest is paid on almost all savings accounts, but understanding how to determine simple interest will help you predict your prospective profits.

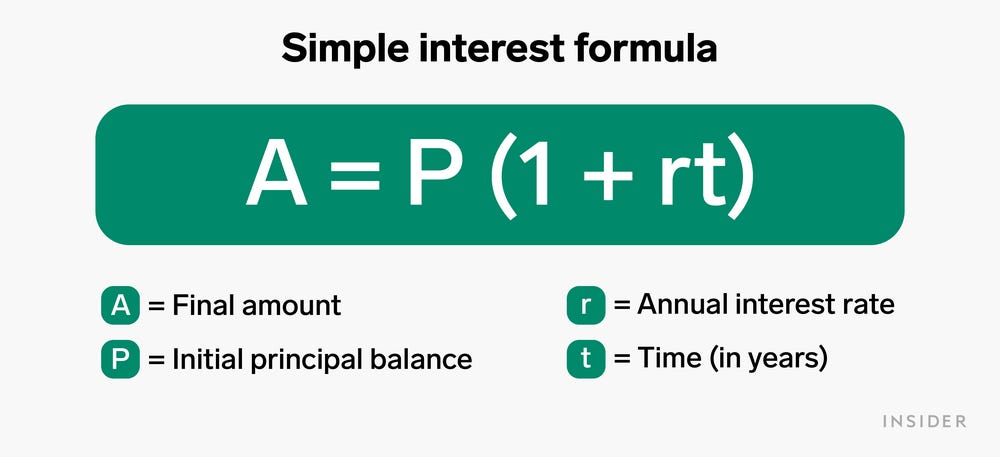

Simple Interest

Earnings on a savings or checking account are said to be "simple" if interest is calculated exclusively on the principal balance. With simple interest, your savings account would accrue interest, but that interest would remain static and never increase. If you deposited $10,000 once in a savings account with a basic 2.00% yearly interest rate, you'd make $200 every year. No interest would be added to the $200 a year you saved. Therefore, after ten years, you would have a balance of $12,000.

Compound Interest

Compound interest has the ability to increase a balance more quickly than simple interest. To put it another way, compound interest is the reason why Albert Einstein called it the "eighth wonder." Interest that is compounded is added to both the principal and any accrued interest. Interest that is compounded is added to your principal amount, as well as any accrued interest. In other terms, both the principal and also the interest accrue on your account. Interest accrues in bank accounts according to the compounding cycle selected.

The frequency with which the financial institution updates your interest balance is known as the compounding period. In most cases, interest on a savings account will be compounded once a month and transferred to your account that same month. By the same token, if the interest rate on a deposit of $10,000 was 2.00% and it was compounded annually, the deposit's balance after ten years would be $12,224 instead of $10,100. That's a positive difference of $214, thanks to the magnifying effect of compound interest.

Calculating Savings Account Interest

To assist you in calculating the amount of interest that will be added to your savings, you may use a savings interest calculator that is available online. Using this technique, you may compute basic savings account interest yourself.

P x R x N = Interest Earned

Hand-calculating these amounts is not without its challenges. Therefore you should probably just use a calculator.

How to Maximize Your Interest Earnings

Here are some suggestions that may increase the interest you get on your savings:

Go Beyond The Bank You Now Use.

The Federal Deposit Insurance Corporation insures online savings accounts to the same extent as those at conventional banks, and the returns they often give are far greater than those of conventional banks.

Think About Opening A Money-Market Account.

If you're able to fulfill the minimum deposit requirement, some banks will give you a better return on your money by placing it in a money market account rather than a standard savings account.

Investigate High-Yield Savings Accounts.

Having a high-yield savings account may significantly accelerate the growth of your interest earnings, but not all financial institutions provide them.

Inquire About Rate Increase Prospects.

Try to find a bank that rewards you with greater interest rates on your savings account if you've reached a particular savings goal, such as keeping a $1,000 amount in the account at all times.

Make Regular Deposits.

With regular deposits, your interest earnings will grow at a rate proportional to the amount of money you have in savings.

Final Thoughts

You have learned the formula for calculating interest on your savings account and the power of compound interest to increase a sum over time. Do not be afraid to look around at several banks to find one that would provide you with the greatest starting deposit rate. If a bank is willing to reward you for saving money, you may as well get the most for your efforts.