Introduction

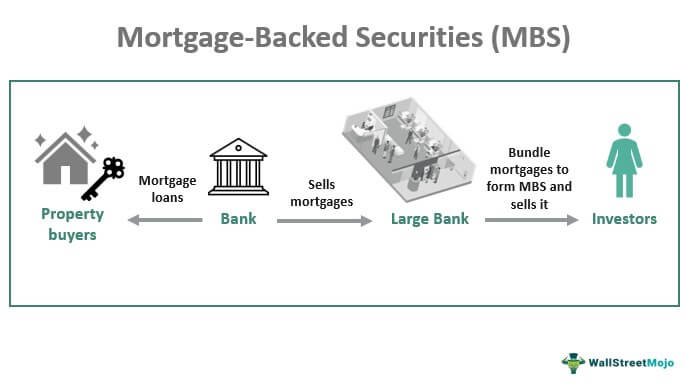

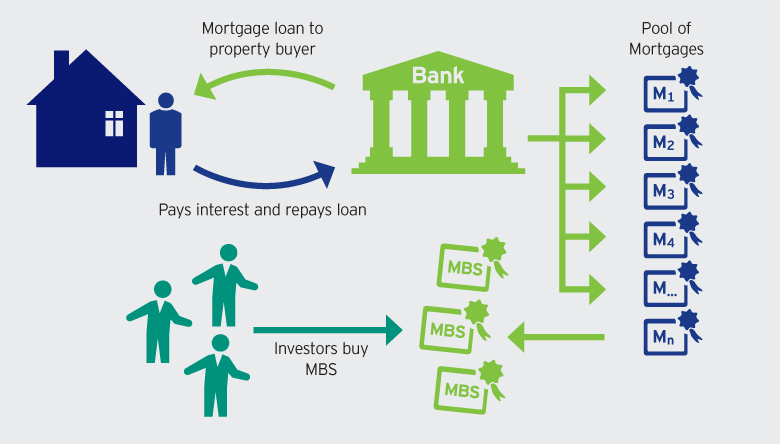

To give one example, mortgage-backed securities are a subset of asset-backed securities. In other words, they are a bond secured by a piece of property, such as a house. 1 The investor is essentially taking over the lender's role by purchasing the mortgage in exchange for monthly payments. Institutional, corporate, and individual investors are the norm for these securities. An investor who bought Mortgage-Backed Securities (MBS) risks losing money if the homeowner defaults on the mortgage.

How a Mortgage-Backed Security Works

Modern mortgage-backed securities were made possible when President Lyndon Johnson signed the 1968 Housing and Urban Development Act, which also established Ginnie Mae. Johnson proposed allowing banks to dispose of mortgages through sales, freeing up capital for other home loans. Thanks to mortgage-backed securities, non-bank financial institutions could enter the mortgage market. Only banks could afford to make long-term loans before MBSs became popular. They were financially stable enough to sit tight until the loans were repaid 15 or 30 years from now.

Lenders could quickly recoup their losses thanks to MBSs, which were first developed to facilitate immediate cash returns from secondary market investors to lenders. Lender participation rose. There were mortgages available that didn't care about the borrower's income or property. Because of this, there is now more competition for conventional banking institutions. As a result, they lowered their standards to remain competitive.

Types of Mortgage-Backed Securities

Mortgage-backed securities come in a few different flavours, but they're all essentially the same thing: bonds. Here are the different types of Mortgage-Backed Securities (MBS).

Pass-Through Participation Certificate

The pass-through participation certificate is the most elementary type of MBS. Mortgage holders get their proportional share of principal and interest payments.

Collateralized Debt Obligation

The market for structured securities became highly aggressive in the early 2000s. To woo new customers, investment banks developed increasingly complex investment products. Collateralized debt obligations (CDOs) were created as examples; they can consist of various loans. These products, which may or may not include mortgages, serve the same purpose for the investor as MBS. Around the time CDOs were created, investment.

Additionally, investment banks created a more intricate mortgage-backed security known as the collateralized mortgage obligation (CMOS). To make these complex investments, a pool of mortgages is divided into segments with similar levels of risk. Regarding default risk and cash flows, the least risky tranches have more certainty, while the riskiest tranches have more uncertainty. Some investors are drawn to the higher interest rates with this increased risk.

Mortgage-Backed Securities: Pros And Cons

Buying mortgage-backed securities is an excellent way to spread risk across a broader range of assets. As an investment that pays out regularly, they may interest those seeking a regular income stream. However, the amounts of these distributions vary, which isn't ideal for investors looking for a steady income stream. Risks associated with collateralized mortgages also apply to MBSs. As a result of refinancing, homeowners may pay back investors their principal amount earlier than expected. Market and liquidity risk are also on the table when purchasing an MBS.

MBS and the Financial Crisis

Mortgage-backed securities were instrumental in triggering the global financial crisis of 2007 that wiped out trillions of dollars in wealth, led to the collapse of Lehman Brothers, and sent shock waves through global financial markets. The rapid rise in home prices and the increasing demand for MBS made it inevitable that banks would relax their lending standards, prompting consumers to rush into the market regardless of the cost.

The Crisis

The origin of subprime MBS can be traced back to that point. As Freddie Mac and Fannie Mae bolstered the mortgage market aggressively, the demand for mortgage-backed securities deteriorated, and ratings became meaningless. Then in 2006, housing costs reached an all-time high. The failure of subprime borrowers to make loan repayments, or "default," became widespread. Because of this, the housing market started its long decline. Foreclosures increased as homeowners realized their properties were worth less than their mortgages.

The value of conventional mortgages, which underpin the MBS market, also fell sharply. Many MBSs and CDOs based on pools of mortgages were grossly overvalued because of the tidal wave of defaults. Losses accumulated as banks and other institutional investors attempted and failed to sell off their bad Mortgage-Backed Securities (MBS) investments. As a result of the subsequent tightening of credit, several banks and other financial institutions came dangerously close to collapse. Because of the halt in lending, the entire economy nearly crashed.

Conclusion

Mortgage-backed securities are sophisticated investments that call for extensive preparation. It would help to verify that the seller is reliable before making purchases. Consulting a financial advisor may be wise if you need assistance finding an MBS that can generate the returns you require. Furthermore, you'll need a sizable sum to purchase an MBS, making these bonds challenging for novice investors. The purchase and sale of mortgage-backed securities continue to this day. Since most people, if given a chance, will opt to keep their current mortgage, the market for such products has revived. The Fed continues to hold a sizable share of the MBS market, albeit one it is working to reduce through incremental sales.